Lessons from the East can help the global FS industry weather history’s perfect storm

Blog: Capgemini CTO Blog

American Founding Father, Benjamin Franklin, has been credited with the aphorism …

… If you fail to prepare, you are preparing to fail.

The COVID-19 virus is a bitter reminder that firms must proactively and preemptively build operational and business resilience to protect against unforeseeable circumstances or force majeure. There is no infallible playbook for quick recovery from a pandemic, and executives are making decisions based on imperfect information. But life must go on! As a starting point, the financial services (FS) industry may undergo an 18% hike in coronavirus-linked operating costs and a 107% decline in operating profits in Q2 2020, according to NelsonHall.

A longtime hotbed for disaster and epidemic, APAC countries have learned to counter tragedy through pre-established recovery and crisis-management techniques. Within today’s coronavirus scenario, let us examine how Asia is maintaining its footing as we all brace for ongoing pandemic impact.

Three pillars support Asian financial institution resilience, according to impact assessments:

- Mitigate business-as-usual impact.

- Adapt to the new market reality.

- Fulfill social responsibility.

1. Maintain business as usual within new normal parameters

Robust digital capabilities help firms accommodate customer preferences and emotional states of mind

As quarantined consumers in Asia stayed home to minimize social contact, digital infrastructure worked overtime to satisfy demand. FS providers maintained business as usual by leveraging online channels for sales, marketing, distribution, and customer engagement.

Capgemini conducted a survey (of more than 11,000 customers across 11 countries) at the peak of the crisis in April and found that more than half of respondents prefer digital over traditional channels for their financial needs. Read our research note “COVID-19 and the financial services consumer” to get more insights from the survey.

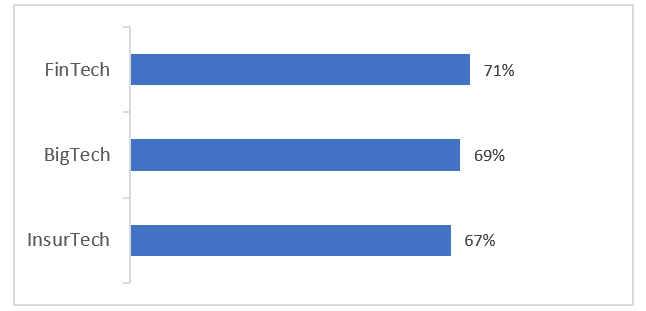

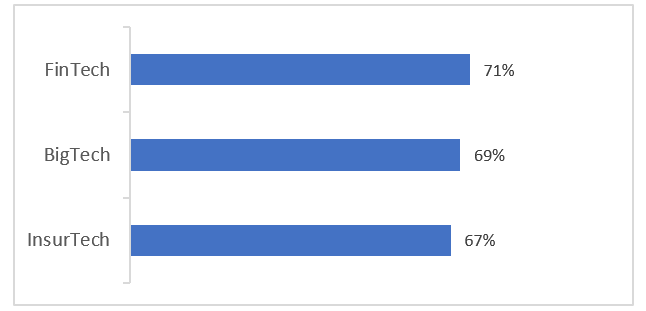

And throughout China and India, the majority of respondents were clear about their willingness to switch to an alternative firm if their current primary banking/financial services provider did not meet their digital requirements (see figure).

Figure: Respondents who may opt for an alternate FS firm

China’s FS sector experienced 100%–900% spikes in critical digital channel traffic during the height of the outbreak. Korea’s Shinhan Bank directed 150 call center staff to work remotely to handle those activities that did not require access to customer information.

Mumbai-based ICICI Bank launched a WhatsApp-based service that enables customers to access essential information/activity such as their account balance or last three transactions, branch and ATM locations, loan offer details, and how to block/unblock credit and debit cards. Singapore’s multinational DBS Bank offered a comprehensive suite of trade financing digital solutions to relieve commercial clients from submitting paper applications for letters of credit, import bills, trust receipts, and bankers and shipping guarantees.

Technology saves the day amid turbulence

The operational resilience of these Asian firms stems from their scalability and a robust digital infrastructure that they built strategically over time. APAC banks rely heavily on digital channels, and therefore branch closures were less consequential than in other parts of the world. As a result, they were ready for business as usual at the first sign of economic recovery.

Indian bank Kotak Mahindra had a detailed business continuity plan (BCP) in place to ensure crisis readiness via advanced cloud-based applications, platforms, and infrastructure. While the BCP focused on backend operations, the bank has now upgraded digital offerings and solutions to customers by leveraging WhatsApp banking, AI-based chat, and voice bots.

China and South Korea temporarily took some banknotes out of circulation as a hedge against micro-traces of the coronavirus that might adhere to the paper. And, central banks are contemplating issuing national digital currencies. To ensure continuous cash supply as paper currency from sectors with high virus exposure are withdrawn for destruction, the People’s Bank of China distributed the equivalent of USD85.6 billion in new banknotes since mid-January, in exchange for old coins and banknotes.

2. Adapt to the new market reality

Identify new revenue streams

- In Singapore, DBS is giving a boost to its food and beverage clients with online order and delivery support from startups Oddle and Firstcom. DBS also plans a branded e-menu with integrated shopping cart, order management, and payment gateways.

- In China, Citibank pooled its legal, compliance, and market teams to work on trade transactions by pushing back a payment date to ensure clients had enough money in their account.

- Asian Infrastructure Investment Bank (AIIB), a Beijing-based multilateral development bank, is disbursing public health-related infrastructure loans at reduced interest rates.

- Chennai-based Indian Bank launched a mobile ATM initiative so that consumers may withdraw cash from a site near their homes.

- In the Philippines, RCBC Bank rebranded its mobile point-of-sale device into ATM Go in early 2020 to serve clients in remote areas through partner-merchants, which include rural banks, neighborhood sari-sari convenience stores, drugstores, cooperatives, and microfinance institutions. RCBC also developed a QR code-enabled application to facilitate quick cashless payments.

- Industrial & Commercial Bank of China (ICBC), the nation’s largest lender, has offered relief to about 5% of its small business clients and allocated USD770 million (5.4 billion yuan) to help companies stay afloat during the pandemic. ICBC is approving qualified small business loan applications as soon as they arrive.

Big but fast … in an era of faster payments

While incumbent banks have been responsive in their initiatives and measures, BigTechs have been exceptionally agile in revamping business offerings and strategies. In China, Alipay’s online mutual-aid platform, Xiang Hu Bao, is leveraging its blockchain platform to speed up claims processing, which reduces the need for face-to-face contact.

Tencent has also rolled out several AI-based open-source health tracking codes that help in preliminary COVID-19 testing and facilitate payments. This trend is likely to gain ground, as almost 46% of consumers we surveyed said they would like to make digital payments in the next 6–9 months.

WeSure, Tencent’s insurance platform, swiftly established an emergency response team to provide real-time information to users and introduced multiple insurance plans. WeSure assembled a COVID-19 response team in early January, and by month’s end, offered its first COVID-19 coverage, free, (up to CNY600,000) upon diagnosis. More than 100,000 medical professionals across China signed up for the plan within a week.

Offering a different approach, Alibaba Group is waiving certain merchant platform fees in a gesture of pandemic solidarity. Platform-based players are in a position of strength as their platforms facilitate outreach and agility to offer new solutions. In the long run, ecosystem-based business models will help incumbents sustain market share, according to 90% of banks surveyed as part of the World Payments Report 2019.

FinTechs turn bane into boon

The coronavirus has cast its shadow on FinTechs, too, as the investment scenario turns bleak.  Lower business volumes in industries such as airlines, travel, and hospitality are affecting the revenues of digital players. In India, the digital payments sector registered a decline of around 30% in transaction value over the past few weeks.

Lower business volumes in industries such as airlines, travel, and hospitality are affecting the revenues of digital players. In India, the digital payments sector registered a decline of around 30% in transaction value over the past few weeks.

In China, 78% of FinTechs said that they responded to the pandemic through R&D of new products and services or technology upgrades (66%). And, more than 50% of FinTech firms offered services to small and medium enterprises (SMEs), according to a survey conducted in February and March by WeiyangX and Tsinghua University’s Institute for Fintech Research.

3. Fulfill social responsibility

Contributions from private-sector players – ranging from social media through philanthropic initiatives and policymaking – have been vital to Asian resilience.

Public-private partnerships have proved their strength in China. For example, Alipay established a program in which more than 1,200 developers jumped on board and devised 181 mini-programs with contactless solutions that could help with grocery deliveries, legal and medical advice, logistics, and public services across China.

Major Asian banks are working directly with governments, regulators, and healthcare institutions to develop and deploy solutions/services for the broader public good. A proposal by State Bank of India (SBI) for interventions to bolster economic liquidity is a strong example. Measures that support society in times of need go a long way in helping firms emerge from crises with strong brand perception.

India-based unicorn Paytm pledged INR500 crores (USD6 billion) to a government-organized pandemic relief fund. To boost spending, the firm also introduced several discount rates for merchants, as well as customer coupons and promotions.

After the storm

As financial institutions everywhere work fervently to devise robust mechanisms that bolster operational and business resilience, financial institutions in China and throughout Asia have already deployed initiatives such as scenario-testing, reformed credit underwriting strategies, better provisioning, and rigorous risk assessment (among others), that can be modeled by other geographies.

Globally, these developments mark a post-COVID new beginning for financial services:

- The sector will undergo a paradigm shift to fully digital.

- New-age players will challenge incumbents in pursuit of the new-digital

- Financial institutions will look to FinTech firms for capability enhancements.

- Digital mastery will emerge as the ultimate FS survival enabler.

- Players that strategically embrace the power of platforms will have an advantage.

Stay tuned for our upcoming research note: “COVID-19_Weathering the Storm” to get a global and pan-sector view.

To learn more about how Capgemini can help, please click here or reach out to Elias Ghanem, Manoj Khera, Sudhir Pai, and Kimberly Douglas to discuss this topic further.

Leave a Comment

You must be logged in to post a comment.