Everything will change, starting with consumer behavior and expectations toward FS providers

Blog: Capgemini CTO Blog

The coronavirus is shaping consumer behavior and business responses across the globe. As we write, more than two billion people are confined at home and reliant on smartphones and laptops to connect  with the outside world. The lucky few have balconies, patios, or a backyard garden, but overall, we are separated from our preferred financial services providers. As countries calculate the economic impact of this black swan event, consumer reaction is triggering change across industries.

with the outside world. The lucky few have balconies, patios, or a backyard garden, but overall, we are separated from our preferred financial services providers. As countries calculate the economic impact of this black swan event, consumer reaction is triggering change across industries.

Full digital may be the big winner as remote work, home delivery (ordered and tracked through mobile apps), virtual meetings, and online training are significantly boosting the adoption of and dependence upon digital handsets. Telecom and tech industries are working to keep up with a sharp spike in demand for remote interactions. And although COVID-19 may have forced organizers to cancel the annual Mobile World Congress, mobile has become global as virtual webinars replace all congresses and trade events.

Whether or not they had tried it before, shoppers everywhere have become e-commerce fans as physical stores and crowded markets are deemed off-limits. But what about consumer behavior toward financial services (FS)?

No immunity for financial services

Like all brick-and-mortar industries, FS is treading uncharted coronavirus waters. A sharp decline in branch visits and an exponential jump in virtual interactions have thrust the digital capabilities and customer experiences of banks and insurers under a glaring spotlight. The already-ongoing global adoption of digital banking and insurance is now on steroids as the pandemic reinforces the criticality of fast, secure, straightforward access to funds, protection, assurance, and financial information.

Individuals, governments, and businesses are embracing digital payments — a behavior change likely to continue once the crisis is over. Consumers have shifted their financial interactions to online channels. They are making insurance claims through self-service mobile apps, meeting remotely with investment advisors, paying for everything either through virtual cards (as much as they can without leaving home), or with plastic in hand during short visits to the essential stores that remain open.

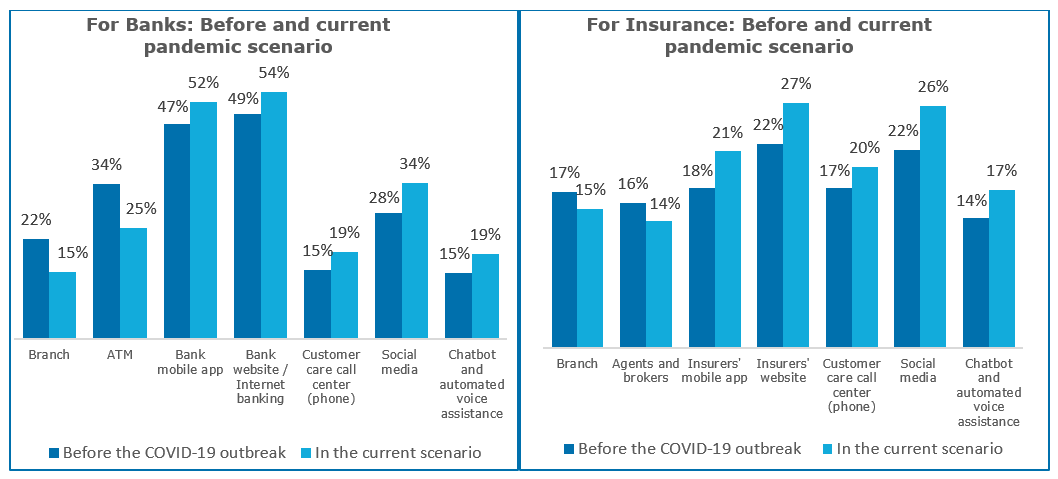

More than half of the respondents to a recent Capgemini Consumer Behavior Survey, conducted in April 2020 with more 11,000 respondents as a part of detailed analysis “COVID-19 and the financial services consumer,” said they favored digital channels. More than 52% said they prefer self-service bank mobile apps during the COVID-19 outbreak compared with 47% before the pandemic. Similarly, 54% said they are conducting bank transactions over the internet during the pandemic, a five percentage point jump over the pre-coronavirus crisis. For the insurance sector, channels such as the firm’s website (27%) and social media (26%) remained the top interaction choices for policyholders – a noticeable jump in numbers in comparison to before the COVID-19 scenario.

Will the contactless modus operandi ignite a cashless payment surge?

Across the globe, banks have temporarily closed branches, and face-to-face retail operations have scaled down dramatically, if not vanished. To minimize one-on-one contact, banks, governments, regulators, and banking associations are encouraging customers to use contact-free digital services.

- The World Health Organization (WHO) recommended contactless payments versus cash, if possible, as a way to limit the spread of the virus that may linger on paper currency.

- Some countries have been exceptionally diligent.

- South Korea is burning cash to prevent the spread of the coronavirus.

- In China, banks are using ultraviolet light or high temperatures to disinfect Yuan bills and then sealing and storing the cash for one to two weeks before recirculation, depending on the severity of the outbreak in a particular region.

FS firms offer waivers, donate services and business continuity support

In the wake of the coronavirus outbreak, banks and insurers, FinTechs, InsurTechs, and BigTechs are stepping up – worldwide – with new solutions such as expanding their digital services portfolios, waiving charges on digital transactions, or offering a moratorium on loan or insurance coverage payments.

In India, ICICI Bank launched ICICI Stack, a digital platform that offers nearly 500 services from retailers, FinTechs, and e-commerce merchants. China’s Ant Financial plans to open its payments platform, Alipay, to third parties to provide business continuity during emergencies and to become a part of customers’ digital lifestyle.

| Focus area | Financial institution | Initiatives |

| Contactless banking | DBS (Singapore) | DBS has digitalized common trade financing processes to reduce reliance on physical over-the-counter exchanges and is offering free FAST transactions to cut the need for physical check handling. |

| Allied Irish Banks (AIB – Ireland) | AIB has rescinded plans to charge for contactless payments to encourage people to adopt contactless banking solutions. | |

| New/advanced digital offerings | Capital One (US) | Capital One encourages customers to use its mobile apps for self-service banking and 24/7 account access. |

Citigroup (US) is pushing proactive reminders and helpful instructions to customers about mobile and digital banking services. In China, Tencent’s insurance platform, WeSure, assembled a coronavirus response team in early January, and by month’s end, offered its first COVID-19 coverage, free, to front-line medical workers, offering up to CNY600,000 upon diagnosis. Other banks are taking steps such as fee waivers, payment deferrals, and loan modifications in response to customers’ changing circumstances. Insurers are also waiving out-of-pocket costs for treatment related to coronavirus. Many financial institutions offer community aid, donations, and healthcare support to help overcome this crisis.

| Focus area | Financial institution | Initiatives |

| Community aid |

China Construction Bank (US) | The US-based online bank is donating $3 million worth of support to communities in need during the pandemic. |

| Bank of America (US) | Bank of America is supporting communities through a $100 million donation. | |

| Waived charges, a moratorium on loan EMIs, etc. |

BMO Harris (US) | US-based BMO Harris is offering waivers for savings and checking account holders for up to two months. |

| NAB, Westpac, Commonwealth Bank, ANZ (Australia) | Following an Australian Banking Association directive, some banks are allowing a six-month deferral on various loan repayments such as mortgages. |

FS firms are clearly feeling the impact of a rapid shift in consumer demand for digital financial services and are stepping up to the challenge. For new-age fully-digital and branchless FS organizations, such as N26, Revolut, or Monzo, the crisis might become a white-swan event (versus the black-swan term used to describe an unexpected disaster) that catapults their digital capability advantage even further.

FS firms are clearly feeling the impact of a rapid shift in consumer demand for digital financial services and are stepping up to the challenge. For new-age fully-digital and branchless FS organizations, such as N26, Revolut, or Monzo, the crisis might become a white-swan event (versus the black-swan term used to describe an unexpected disaster) that catapults their digital capability advantage even further.

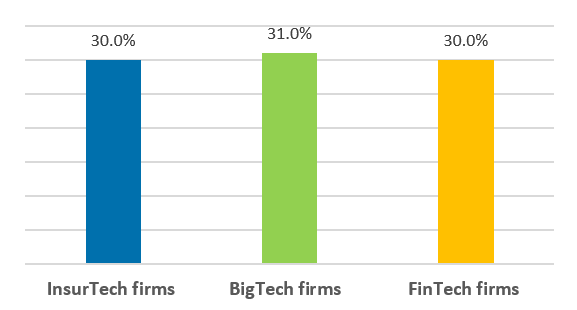

The Capgemini Consumer Behavior Survey revealed that around 30% of bank customers would switch to FinTech firms after the COVID-19 pandemic if their primary financial provider failed to deliver the customer experience (CX) they expect. Similarly, 30% of insurance customers said they were inclined to switch from their existing provider to an InsurTech if CX came up short.

However, gaps remain and, in some cases, are expanding when it comes to delivering a seamless and integrated banking experience. Capgemini’s World Retail Banking Report 2019 found that only 31% of customers said their banks provided access to a variety of useful financial apps, and only 41% said they had the flexibility to make payments on any platform.

The need of the hour: Address FS customers’ end-to-end needs – DIGITALLY

Traditional customer touchpoint channels are running out of steam. JPMorgan Chase temporarily closed approximately 1,000 branches in early March – around 20% of its total footprint – to protect employees, yet continued to provide essential services to its customers and communities. Traditional channels are reporting a decline in use during the pandemic, with only 15% of customers saying they prefer branch banking as an interaction point within the virus scenario – a significant reduction of seven percentage points compared with the 22% choosing a branch visit before the crisis.

Will the surge in digital activity push firms to rethink strategy, business models?

Customers’ often urgent coronavirus-related inquiries have overwhelmed FS support channels – online, email, and phone – to unequivocally illustrate the unprecedented need for a digitally connected ecosystem. Widespread adoption of new-age digital channels such as chatbots, automated voice assistants, and social media tools appears inevitable.

Results from our consumer behavior survey support this observation as 34% of banking users said they preferred social media as an interaction channel during the pandemic versus 28% before the virus. Responses for chatbots and automated voice assistance revealed a similar pattern, with 19% of consumers saying they prefer automated communication tools now compared with 15% before the crisis.

Throughout the unpredictable weeks and months ahead, the crisis-sparked surge in digital activity is bound to generate new customer habits that require banks and insurers to function online. Ultimately, will full digital rein as the exclusive customer engagement channel? Unlikely, but it may become the primary channel customers use to engage. Each day of confinement promotes digital use. And that begs the question – Are FS incumbents ready to prioritize digital capabilities and offerings for success in a virtual world?

For more insights on the changing customer behavior in financial services refer to the detailed research note “COVID-19 and the financial services consumer: Supporting customers and driving engagement through the pandemic and beyond.”

To learn about how Capgemini can help, please click here or reach out directly to Elias Ghanem, Sankar Krishnan, and Julien Assouline to discuss this topic further.

Leave a Comment

You must be logged in to post a comment.