5 Steps for Reducing Your Risk of Check Fraud

Blog: Kofax - Smart Process automation

To pay or not to pay…that is the question financial institutions are under intense pressure to answer when it comes to evaluating the legitimacy of checks.  The answer can be complicated in a world where banks must balance high customer expectations, regulatory compliance and cost pressures—all while protecting themselves from increasingly savvy fraudsters.

The answer can be complicated in a world where banks must balance high customer expectations, regulatory compliance and cost pressures—all while protecting themselves from increasingly savvy fraudsters.

Yes, consumers are still writing checks

It might surprise you to learn that although the use of paper checks is declining in the U.S., checks still account for a large portion of the total number of payment transactions, particularly in business-to-business (B2B) dealings. More than 12 billion checks were written in the U.S. in 2015, and one-third of all payment transactions in the U.S. in that year were based on checks.[1] The number in the U.K. is lower, but still significant: 546 million checks were used to make payments in 2015, and approximately 237 million checks are expected to be used to make payments in 2025.[2]

However, since there is an overall decline in the number of checks in circulation, there must be fewer instances of check fraud, right? Unfortunately, no. Consider that in the U.S. alone, the number of check fraud cases jumped by 19% between 2012 and 2014.

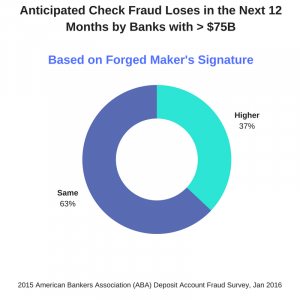

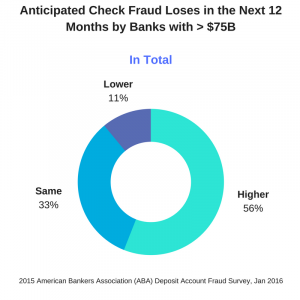

The surge in mobile check deposits only complicates the situation. Existing systems often have trouble detecting counterfeit and altered checks or forged signatures from scanned images. Currently, two-thirds of losses still originate from over-the-counter items. However, remote deposit capture already accounts for 12% of losses due to fraud, and as banks continue to see customers adopt mobile-friendly applications, losses attributed to remote deposit capture can be expected to grow.[3]

Checks—a path of least resistance for fraudsters

With so many still in circulation, checks continue to be the payment method most targeted for fraud.[4]  A recent survey concluded that there are more than 1,500 cases of check fraud in the U.S. every day.[5] On an annual basis, the U.K. is seeing fewer cases of check fraud compared to the U.S. (approximately 5,746 versus 565,303 cases per year) 6, 7, but is experiencing higher average losses per item. Counterfeits were the major source of fraud losses for U.K. banks in 2015, with a significant 41% increase compared to 2014.8 And although many U.K. banks have strong check fraud detection systems in place, the number of cases is expected to rise when the U.K. introduces mobile deposits on a broader scale in 2017, which will challenge these defense lines.9

A recent survey concluded that there are more than 1,500 cases of check fraud in the U.S. every day.[5] On an annual basis, the U.K. is seeing fewer cases of check fraud compared to the U.S. (approximately 5,746 versus 565,303 cases per year) 6, 7, but is experiencing higher average losses per item. Counterfeits were the major source of fraud losses for U.K. banks in 2015, with a significant 41% increase compared to 2014.8 And although many U.K. banks have strong check fraud detection systems in place, the number of cases is expected to rise when the U.K. introduces mobile deposits on a broader scale in 2017, which will challenge these defense lines.9

Some banks have focused on tightening their security around other payment forms, like credit cards, but many haven’t paid much attention to checks because they were hoping that check usage would decline much faster than it has.  This has left many banks vulnerable and weakened consumers’ trust in the security of payment processing. They expect quick access to their funds, so banks must be able to identify suspected fraud immediately and put non-suspicious items on the fast track for payment.

This has left many banks vulnerable and weakened consumers’ trust in the security of payment processing. They expect quick access to their funds, so banks must be able to identify suspected fraud immediately and put non-suspicious items on the fast track for payment.

Key line of defense against fraud—take a holistic approach

So what should you look for when evaluating a check fraud solution that will protect you from losses and keep your customers happy?

First, here’s what not to do: many banks use simple processing rules (high-dollar threshold, etc.) and behavioral pattern monitoring, along with a team of visual inspection processors, or fraud analysts. These methods tend to produce a high number of false positives and, in most cases, don’t reduce fraud loss to an acceptable level.

For the most comprehensive fraud protection, choose a solution that considers a number of weighted factors, including comparing the handwritten check signature to the reference signature on file, leveraging information from external systems, identifying discrepancies in check stock, determining whether or not an item is pre-authorized, and verifying the payee is on a bank-specified white or black list. You can then use a “combined risk score” to assess the level of risk and make a pay/no pay decision.

5-step approach for reducing your risk of fraud

Don’t leave a gap—or worse, a gaping hole—in your check fraud detection system. Look for a holistic solution that takes a multi-step approach for operational risk mitigation.

Below is a commonly used and successful approach:

- Build up customer profiles; fully automate them, if possible.

- Use image-based detection engines that fit actual fraud exposure, including automatic signature verification.

- Combine all information from these image engines, and then plug in external scoring data and parallel data analysis into the “combined risk scoring” engine.

- Create and maintain fraud rules, ideally in a Combined Risk Score editor, to match concentrated information with current exposure patterns.

- Retrofit fraud findings and good customer behavior patterns back into the profiles.

To learn more about check fraud detection and signature verification, we invite you to view a recording of a recent American Banker webinar Defend against check fraud with e-signatures and signature verification.

Sources:

[1] Bank of International Settlements (BIS), Statistics on payment & settlement systems in selected countries, “Red Book,” Sep 2016

[2] Payments UK – 2016 UK Payment Markets – Summary

[3] 5, 7 & 8 2015 American Bankers Association (ABA) Deposit Account Fraud Survey, January 2016

[4] Association for Fraud Professionals (AFP) Payments Fraud and Control Survey, published March 2016

6 Year-End 2015 Fraud Update, Financial Fraud Action UK

9 2016 Fraud the Facts, Financial Fraud Action UK

Leave a Comment

You must be logged in to post a comment.