#Fintech Disruption in Banking – Will Neo Banking be the new normal in COVID Era?

Blog: NASSCOM Official Blog

The global banking sector is increasingly being disrupted by a new wave of FinTech – The Neo banks – that have challenged every part of the traditional banking model, from customer onboarding to transaction models, to consumer marketing, etc. magnifying the competition in a big way.

Neo (new) banks are FinTechs that are the new-age interpretation of banking services.

In contrast to the conventional banks, which may offer digital services, but usually rely on their physical branches, neo-banks are digital-only financial institutions. Neo banks do not have a physical presence. Every process is digitized, and everything can be done from the bank’s website or just a smartphone app.

Globally, neo banking has recorded a CAGR of 50.6% from 2016 to 2020 being valued at US$ 50.2 million in 2020. Further, it is forecasted to grow at a similar pace to reach a market size as huge as $394.6 billion by 2026.

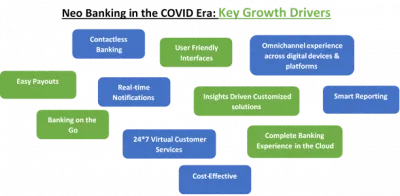

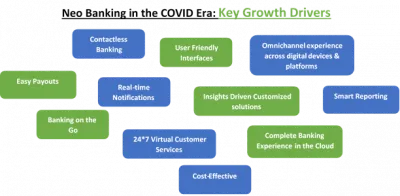

Key Benefits of Neo Banks:

Neo Banks with their digital-only presence offer a range of benefits that bridge the gaps in the age-old banking models of traditional banks. These in turn act as the key growth drivers of Neo Banking globally

Some of the Top Global Neo Banking Fintech Players that are supporting customers through their digital banking solutions during COVID-19 include, UK-based Atom Bank, Tandem, Monzo Bank, & Starling Bank, Brazil-based Nubank – that provides 100% digital services, including digital accounts, international credit card, and personal loans, & Xinja – an Australia-based neo bank that offers financial management, home loans, debit cards, and prepaid cards, etc., among many others.

Neo-Banking in India:

India too is not left behind in the neo-banking arena and the country has seen many such players budding over the last few years, with the COVID crisis only boosting the market for such FinTechs.

These include both funded and non-funded neo banking FinTechs. Currently, there are around 27 active Internet- First Banks (Neo-Banks) in India with a total VC funding amounting to US $ 111 million-plus. Further, the total funding in neo-banks has only seen an increasing trend over the last 2 years.

Some of the leading Neo-Banking player examples in India include Bangalore based – Open, which prides itself to be Asia’s first neo banking platform for SME businesses.

Other Top Neo- banking players in India include names like Hop, Pink Capital, epiFi, YeloBank, PayZello – neo banks for consumers, PayO – a Bangalore-based neo bank for businesses, Vanghee – another neo bank for businesses, Airtel Payments Bank, Paytm Payments Bank, etc.

Though neo-banking in India has been flourishing over the last few years and is expected to leapfrog forward especially in the COVID era, one big constraint for the Neo-Banks in the Indian market is the Indian Regulatory Framework!

Owing to regulatory policies by the RBI that do not recognize or rather deny the legitimacy of digital-only banking institutions (due to its concerns over cryptocurrency transactions), neo banks in India are not strictly 100% digital!

This means, that RBI does not give virtual banking licenses and demands some sort of physical branches from these banks. As a result, many of these internet-first banks are either partnering with those banks that have licenses or are offering only a few banking services like payments, lending (and not savings) (e.g. Airtel payments banks, Paytm Payments Bank). Thus, making the neo-banking story in India, partially incomplete!

Looking Ahead: 2020 & Beyond

Looking ahead, we expect the banking industry in India to see a blended model in the COVID era where Neo Banks and traditional banking giants like ICICI, HDFC, etc. co-exist. With innumerable benefits like customer-centric banking solutions, complete digital models, cost-effectiveness, ease of accessibility, contactless banking, etc., Neo Banks in India are sure to see a huge surge in adoption in 2020, especially among the digitally active Indian users in this COVID-hit era.

Further, considering the regulatory barriers created by RBI in India for Neo Banks to stay on for a while, one of the key models that we expect these neo-banks to continue to explore – is strategic partnerships with established banking giants – to increase their reach, & gain market share in the Indian Banking Industry.

Stay tuned to read more on fintech disruptions. You can also comment in the box below or can reach me here.

About the Author: Shivani is leading FinTech research initiatives at NASSCOM, having close to 12 years of experience in research and consulting in the areas of banking & financial services, FinTech, and related technologies. In her current role at NASSCOM, she is closely working with the industry leaders and other stakeholders in delivering strategic insights on digital transformation and articulating a roadmap in disruptive technologies for the Indian IT and the FinTech industry.

References:

https://fintechstars.wordpress.com/

https://www.televisory.com/blogs/-/blogs/dawn-of-the-digital-banking-neobanks

Zion Market Research

Traxcn

Forbes

Trade Promotion council of India

NASSCOM Insights

The post #Fintech Disruption in Banking – Will Neo Banking be the new normal in COVID Era? appeared first on NASSCOM Community |The Official Community of Indian IT Industry.