Basel IV: Is it still worthwhile to use the IRBA?

Blog: Capgemini CTO Blog

Background CRSA and IRBA

Banks generally use either the Credit Risk Standard Approach (CRSA) or the Internal Ratings Based Approach (IRBA) to determine the capital required for their credit risk. Under the CRSA, risk positions are multiplied by fixed risk weights to calculate risk weighted assets (RWA). In contrast, banks can – given supervisory approval – estimate the exposure at default (EAD), the probability of default (PD) and the loss given default (LGD) using internal models and bank data. Risk weights can be calculated from supervisory formulas based on internally calculated PDs and LGDs. Finally, the exposure amounts at default are multiplied by the calculated risk weights to determine the RWA.

Need for action for banks due to output floor

The finalized Basel III reform, known as “Basel IV”, reduces the capital benefit of the IRBA by introducing an output floor. The following question therefore arises: Does the further use of the IRBA pay off or does a change to the CRSA – especially for cost reasons – show an advantage?

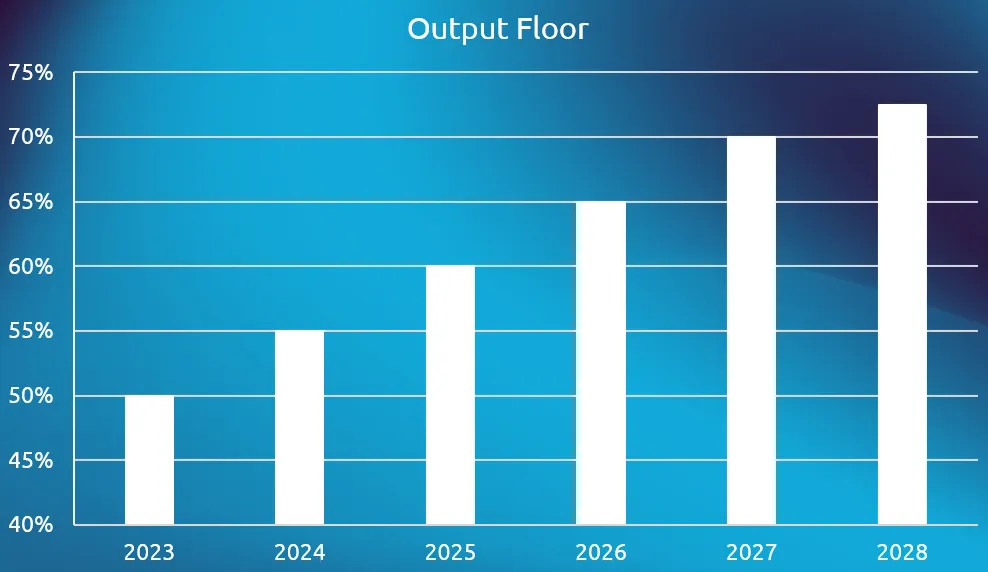

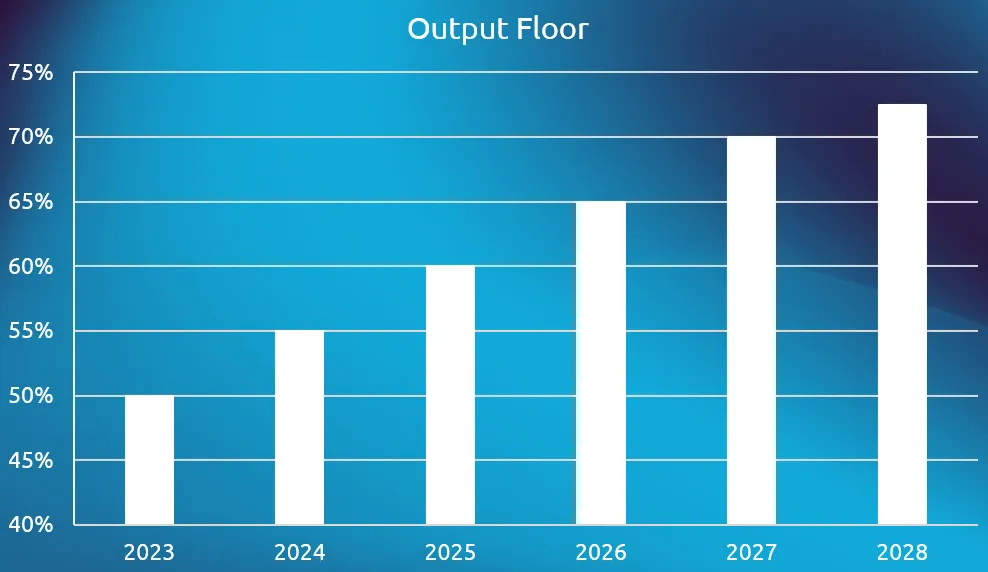

From a regulatory perspective, the intention is to reduce the undesired variability of RWA resulting from different modelling approaches across banks (ECB’s Targeted Review of Internal Models (TRIM) und EBA Report of the 2019 Benchmarking Exercise). For this reason, a so-called “output floor” will be introduced in the course of Basel IV. The RWA calculated on the basis of the IRBA are thus limited to 72.5 % of the RWA calculated according to the CRSA. The output floor will be introduced gradually over five years. As of January 1, 2023, the output floor is 50 % and increases by 5 percentage points per year until 2027, when it is finally raised to 72.5 % in 2028 (s. figure 1).[1]

Figure 1: Illustration of the output floor of total RWA

Quantitative cost-benefit analysis of CRSA and IRBA

In order to answer the question of whether the IRBA is superior to the CRSA in terms of a cost-benefit analysis, two quantitative factors must be considered. First, it is necessary to calculate the capital benefit as the difference between the CRSA and IRBA RWA. As a result of the phased introduction already mentioned, the capital benefit of the IRBA will continue to decrease and will amount to a maximum of 27.5% from 2028 onwards. On the other hand, the use of the much more complex IRBA involves higher operating costs than the CRSA. The higher operating costs are due to personnel costs for model development, validation and verification, the costs of special software solutions and the costs of consulting services. Consequently, banks need to know whether the capital benefit of the IRBA compensates for the higher operating costs involved.

Qualitative analysis of CRSA and RBA

In addition, there are two qualitative factors that play a role in determining whether banks should switch from the IRBA to the CRSA.

- Banks should examine whether supervisors allow to switch to the CRSA. Even if supervisors allow a switch, the use of internal models to determine the probability of default for IFRS 9 accounting purposes remains mandatory. The associated operating costs therefore remain.

- As IRBA banks are more advanced (compared to non-IRBA banks), they should consider the impact of a potential loss of reputation by switching to CRSA. A switch to CRSA may have a negative impact on the bank’s external rating and ultimately worsen the bank’s refinancing conditions.

Outlook

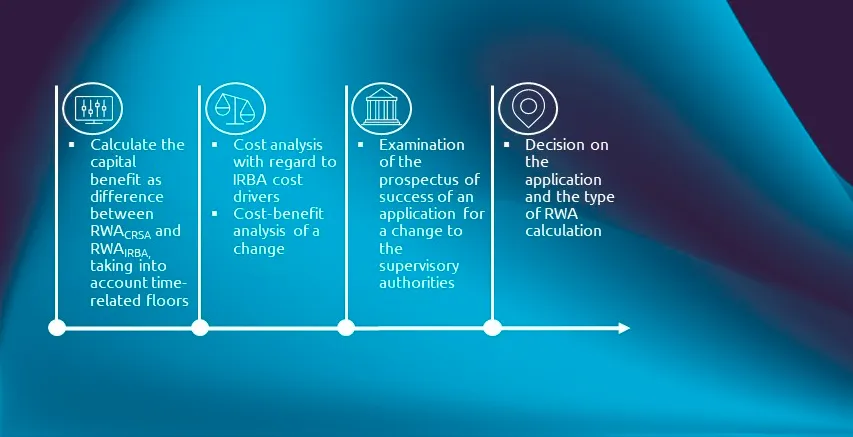

The extent to which a change of approach is worthwhile must be examined by means of a structured cost-benefit analysis (see Figure 2). The necessary calculation of the capital requirements according to CRSA and IRBA is a challenge due to the time and resources required. Ultimately, the benefits of the IRBA depend to a large extent on the bank-specific credit portfolios. For this reason, it is advisable to examine each individual case and ask the experts from the Inventive Finance, Risk & Compliance Team to support you.

Figure 2: Our suggestion for determining the advantageousness of the IRBA

This article is co-authored by Max Müller