Understanding SWIFT: How it powers global payments and why banks are modernizing it

Blog: OpenText Blogs

SWIFT sits at the center of global financial transactions. Financial institutions rely on it every day to send secure, standardized payment messages across borders. But the role of SWIFT is changing. As real-time payments, ISO 20022, and compliance demands accelerate, banks must rethink how they manage SWIFT connectivity and scale operations.

What is SWIFT?

SWIFT (Society for Worldwide Interbank Financial Telecommunication) provides a global messaging network that allows financial institutions to exchange payment instructions securely. SWIFT does not move money. Instead, it sends standardized messages that instruct banks how to process transactions.

More than 11,000 institutions use SWIFT to support cross-border payments, securities transactions, and trade finance operations.

How SWIFT works

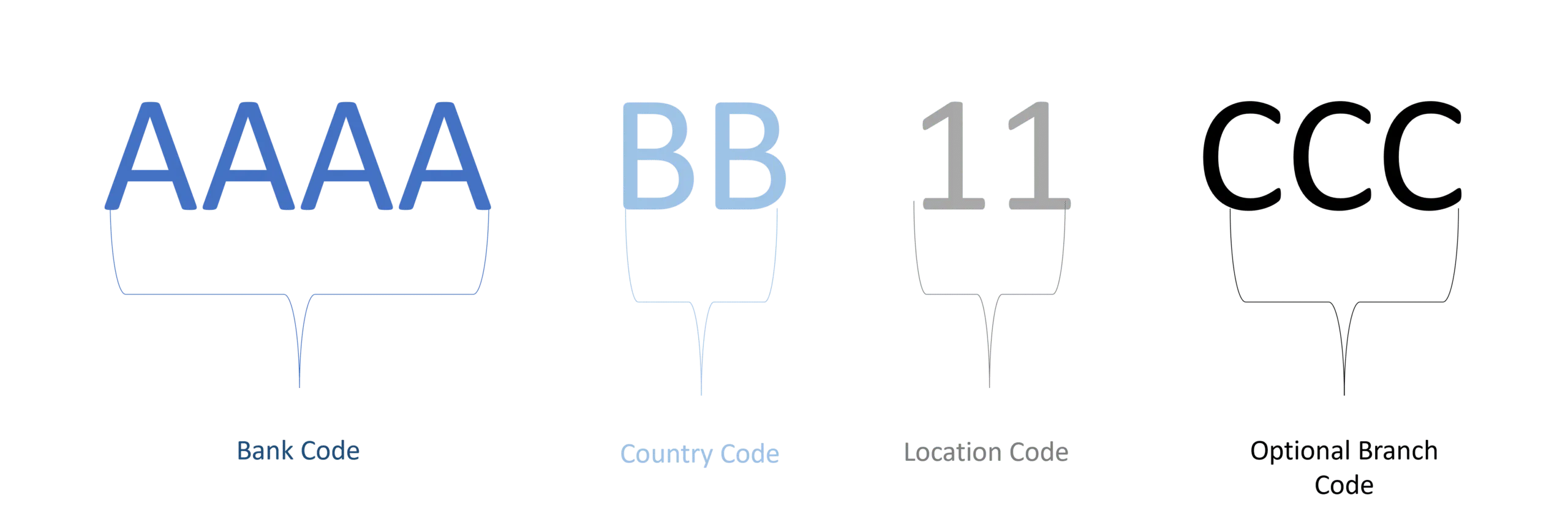

SWIFT connects banks through a secure messaging network. Each institution uses a unique SWIFT code (BIC) to identify itself. A typical SWIFT transaction follows this flow:

- A bank sends a SWIFT message with payment details

- Intermediary banks route the message if needed

- The receiving bank processes the transaction

SWIFT enforces strict standards, which allows institutions to exchange financial data consistently and securely at global scale.

SWIFT remains essential and continues to power global financial messaging because it delivers trusted, secure communication between institutions, standardized formats for consistent processing, and global reach across thousands of banks and markets. However, while SWIFT remains critical, the way banks use it must evolve.

The challenge: Legacy SWIFT environments limit scale

Many banks still manage SWIFT connectivity infrastructure on-premises, which creates significant operational challenges. These environments drive high infrastructure and maintenance costs, limit scalability as transaction volumes grow, and rely on manual onboarding and integration processes. They also slow the adoption of evolving standards such as ISO 20022. As a result, financial institutions struggle to keep pace with real-time payment demands and increasing regulatory expectations.

SWIFT and ISO 20022: A major shift

The move to ISO 20022 fundamentally changes how financial institutions use SWIFT by shifting from simple message exchange to rich, data-driven processing. ISO 20022 introduces structured, standardized data formats that carry significantly more information within each transaction. This enables greater payment transparency, allowing banks and their customers to track and understand transactions with more context and accuracy. It also drives higher levels of automation and straight-through processing, reducing manual intervention and operational friction across payment workflows.

At the same time, richer data improves compliance and reporting by making it easier to screen transactions, detect anomalies, and meet evolving regulatory requirements. Institutions can embed controls such as sanctions screening and validation directly into payment flows, rather than relying on downstream checks.

However, these benefits come with increased complexity. Payment volumes continue to rise, settlement speeds accelerate, and data requirements expand. Banks must process larger, more complex messages in near real time—without introducing errors or delays. Legacy SWIFT environments, which often rely on rigid formats and manual processes, struggle to support these demands. As a result, many institutions must modernize their SWIFT infrastructure to fully realize the value of ISO 20022.

How banks are modernizing SWIFT

Banks no longer treat SWIFT as a standalone system. Instead, they modernize it as part of a broader integrated payments hub strategy that brings together connectivity, processing, and compliance on a single, scalable platform. This shift allows institutions to move away from fragmented, point-to-point integrations and toward a more unified, API-driven architecture.

With this approach, banks can scale bank connectivity solutions across multiple networks and regions, streamline corporate-to-bank integration, and enable both API and EDI-based connectivity to support diverse client needs. They can also standardize and accelerate ISO 20022 transformation across all payment flows, ensuring consistency and interoperability.

By consolidating these capabilities, banks reduce operational complexity, improve agility, and create a foundation that supports real-time payments, faster onboarding, and future innovation.

What a modern SWIFT approach looks like

Cloud-based SWIFT connectivity

Banks replace on-premises infrastructure with secure, managed services that scale globally.

Built-in transformation for ISO 20022

Modern platforms handle message transformation across SWIFT MT, MX, and other formats without manual intervention.

Embedded compliance and risk controls

Banks integrate real-time sanctions screening and monitoring directly into payment workflows.

Faster onboarding and integration

Standardized APIs and EDI connections simplify onboarding for corporates and partners.

Real-time visibility

Teams gain full insight into payment flows, statuses, and exceptions across the SWIFT network.

The business impact of modernizing SWIFT

When banks modernize SWIFT, they can:

- Reduce infrastructure overhead and total cost of ownership

- Scale operations to support real-time payments

- Improve compliance and reduce fraud risk

- Accelerate onboarding and revenue generation

- Deliver better customer experiences with faster, more transparent payments

Most importantly, they shift focus from maintaining infrastructure to driving innovation.

Take the next step with SWIFT

Modernizing SWIFT does not require rebuilding everything from scratch. With the right approach, you can transform your SWIFT environment into a scalable, cloud-first foundation for global payments. Learn how OpenText Service Bureau helps financial institutions simplify SWIFT connectivity, reduce costs, and scale operations with a managed service.

The post Understanding SWIFT: How it powers global payments and why banks are modernizing it appeared first on OpenText Blogs.